REITs

CapitaLand Ascendas REIT's share price slides. Is it a bargain?

By Beansprout • 23 Apr 2024 • 0 min read

CapitaLand Ascendas REIT's share price has fallen by more than 10% year-to-date. We look at its latest business update to find out if the REIT is now a bargain.

In this article

What happened?

The share price of Singapore REITs have been fairly weak recently.

For example, I shared earlier than Keppel DC REIT is trading close to its one-year low after cutting its dividends for the first quarter of 2024.

This comes amidst the expectation that the Fed will keep interest rates higher for longer as inflation remains persistent.

Singapore REITs continue to report their first quarter operational updates, and some investors asked about the performance of CapitaLand Ascendas REIT.

After all, CapitaLand Ascendas REIT was one of the most resilient REITs with positive share price returns in 2023.

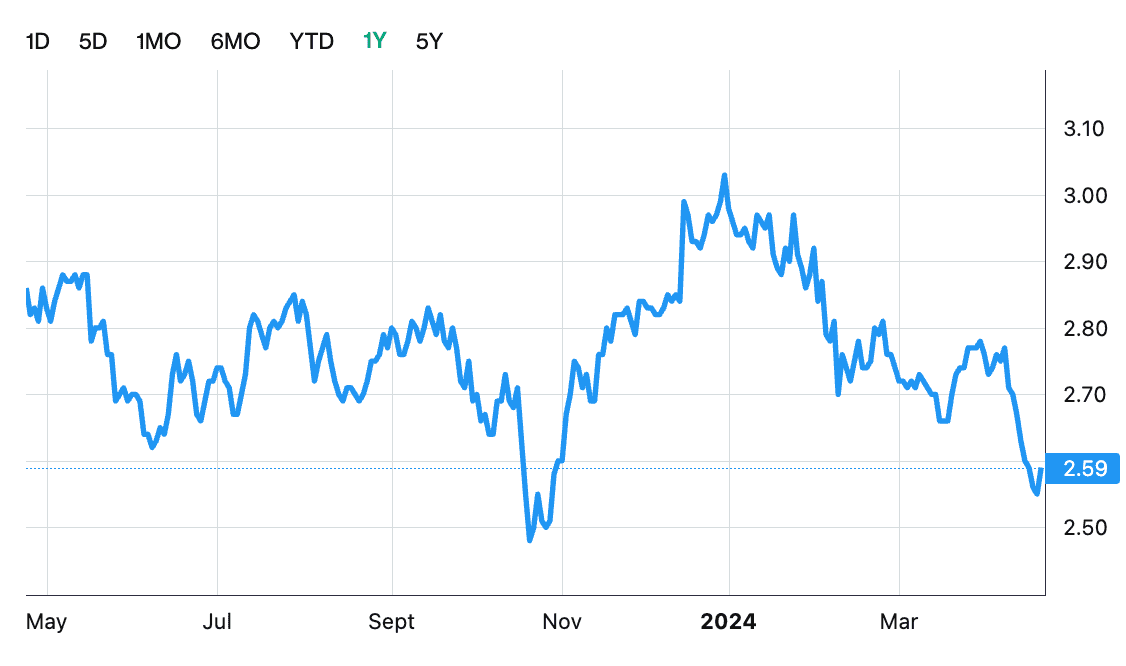

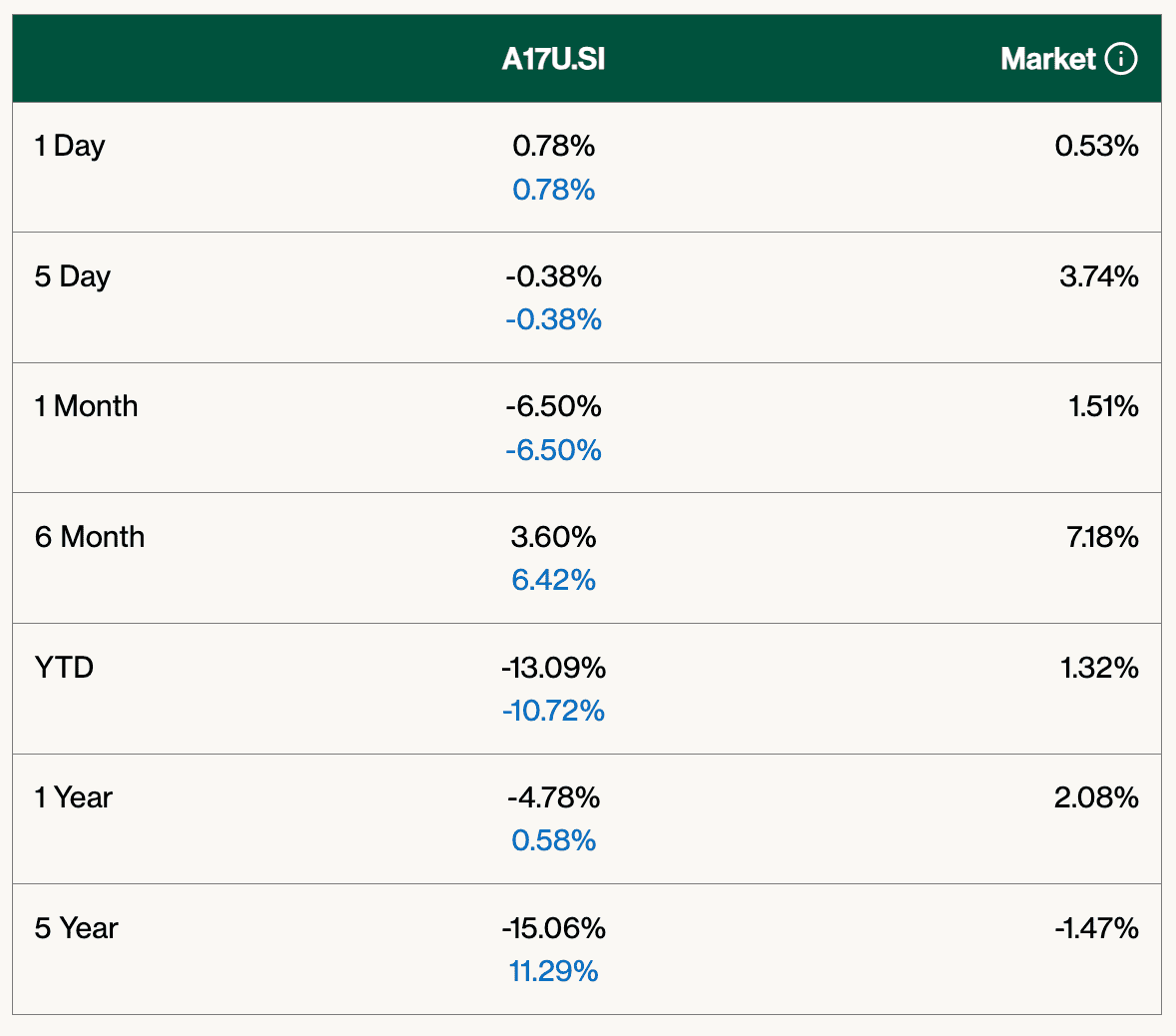

However, CapitaLand Ascendas REIT’s share price has declined by 13% year-to-date to reach S$2.59 as of 23 April.

In this post, I shall be diving deeper into its latest business update to find out what may be driving the weakness in CapitaLand Ascendas REIT’s share price.

What you need to know about CapitaLand Ascendas REIT’s latest business update

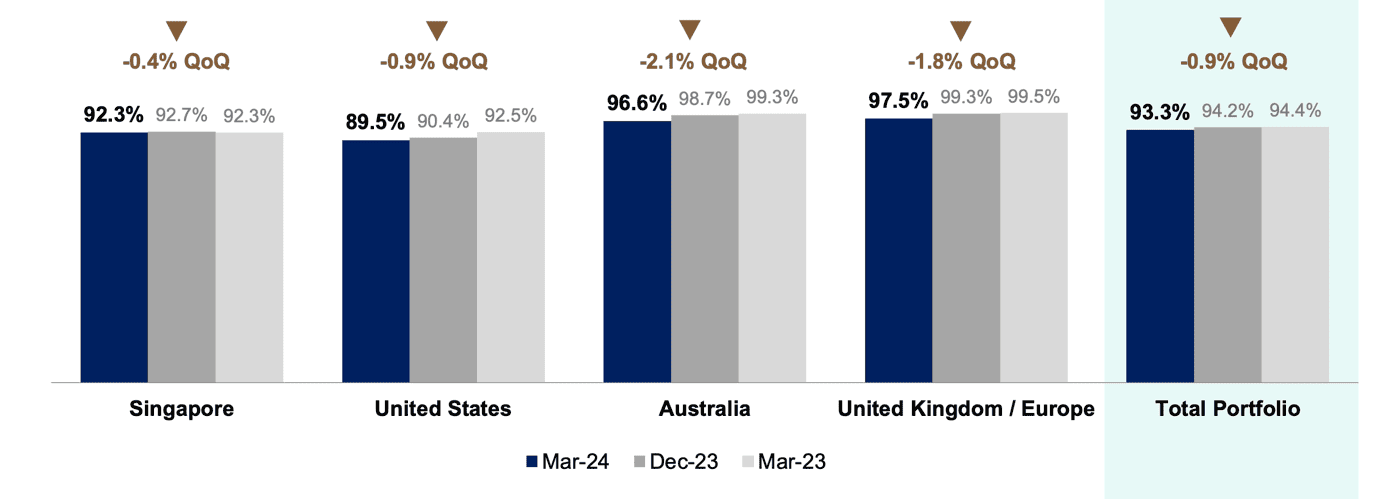

#1 – Slight decline in portfolio occupancy

CLAR’s overall portfolio occupancy stood at 93.3% for 1Q 2024, down slightly from 94.2% in the previous quarter.

Both Australia and the UK/Europe sported high occupancies of 96.6% and 97.5%, respectively.

In contrast, Singapore and the US saw lower occupancies of 92.3% and 89.5%, respectively.

The culprit for the US was Lackman Business Centre, a logistics property in Kansas City, where occupancy fell to 82% from 100% because of a tenant movement.

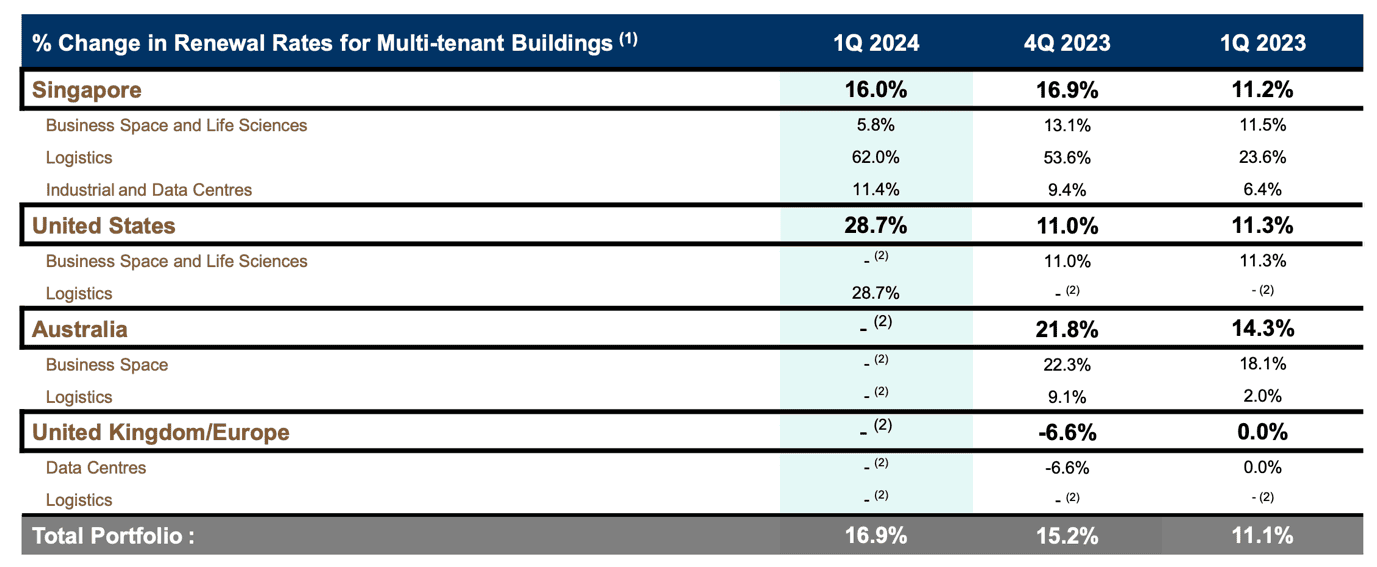

#2 – Continued positive rental reversions

Next, we look at CLAR’s rental reversions.

For this metric, the REIT has an impressive track record with 1Q 2024 displaying a positive rental reversion of 16.9%.

The main contributor was the US which recorded a positive rental reversion of 28.7%.

CLAR has demonstrated positive double-digit rental reversions in the previous quarter and for 1Q 2023, attesting to the strong demand for its industrial properties.

Both the second and third quarters of 2023 also saw double-digit positive rent reversion, making it five quarters in a row with double-digit rent reversions.

For 2024, CLAR expects rental reversions to be in the positive single-digit range.

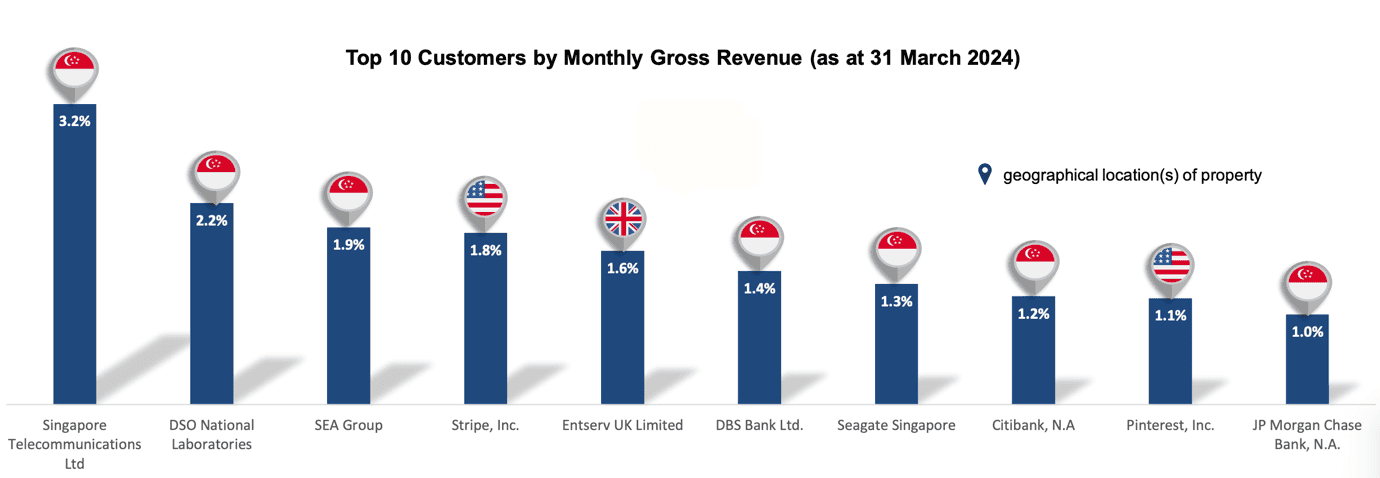

#3 – A diversified customer base

For investors who worry about whether tenant defaults may sink CLAR’s DPU, the above shows how diversified the REIT’s customer base is.

The REIT has around 1,790 tenants and the largest of these, Singtel, only takes up 3.2% of gross revenue.

With the top 10 tenants comprising around 16.7% of the REIT’s monthly revenue, investors need not worry about a sharp fall in DPU should any of them encounter financial trouble.

These tenants are also diversified across more than 20 different industries, with nearly two-thirds of the tenant base in the technology, logistics, and life sciences sectors.

What’s more, any single property does not contribute more than 4% of CLAR’s gross monthly revenue.

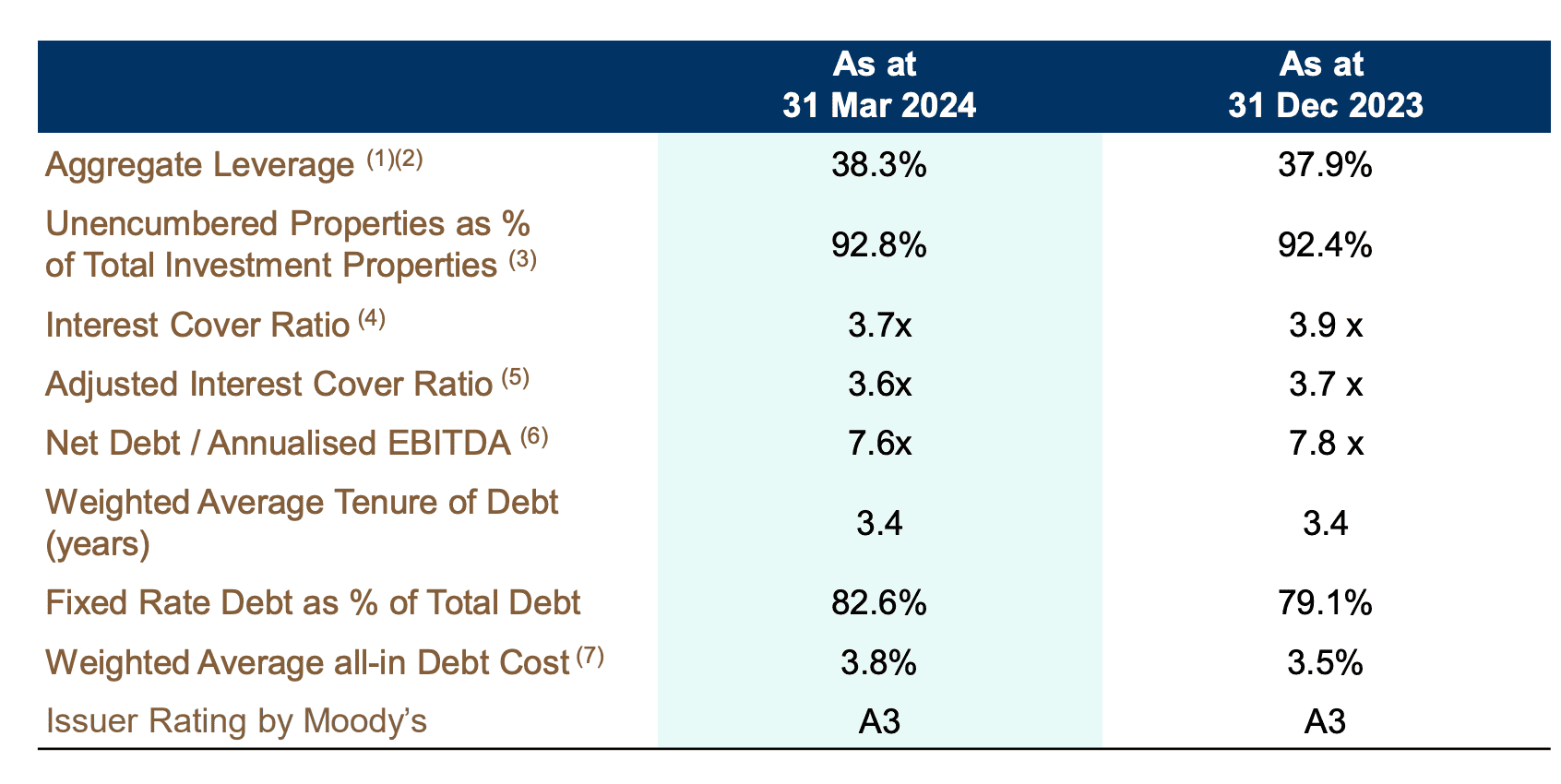

#4 – Healthy debt metrics

Source: CapitaLand Ascendas REIT’s 1Q 2024 Business Update

CLAR’s aggregate leverage stood at 38.3% as of 31 March 2024, slightly higher than the 37.9% logged three months ago.

The REIT’s weighted average all-in cost of borrowing, however, crept up slightly from 3.5% in the previous quarter to 3.8%.

The good news is that CLAR’s interest coverage ratio declined from 3.9x to 3.7x while its fixed rate debt proportion increased from 79.1% to 82.6%.

These are positive signs that the REIT manager is taking proactive steps to mitigate rising interest rates that could crimp DPU.

In addition, CLAR also has a well-spread-out debt maturity profile with not more than one-fifth of its loans coming due in any year.

Moreover, 14% of its debt is due in 2030 and beyond.

The industrial REIT also quantified the effects of a rise in interest rates, stating that a 1% increase in interest rates will negatively impact DPU by just 1.7%.

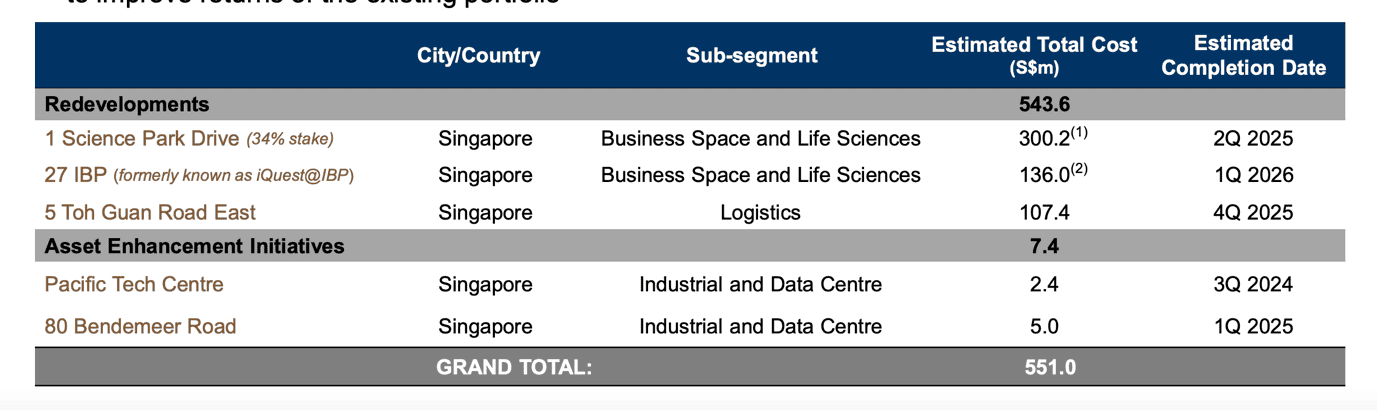

#5 – AEIs to improve portfolio quality

Apart from acquisitions, which are understandably tougher in a high interest rate environment, REITs can choose to renovate or refurbish their properties through asset enhancement initiatives (AEIs).

CLAR has consistently undertaken a series of AEIs over the years to spruce up its portfolio and improve its returns.

The slide above shows a list of five ongoing projects worth S$551 million that are undergoing either redevelopment or refurbishment in Singapore.

As these projects are progressively completed, the REIT should enjoy an uplift in rental income as demand for leasing these properties increases, thereby feeding into more positive rental reversions.

What would Beansprout do?

In my view, CapitaLand Ascendas REIT has continued to deliver a mixed set of numbers in its latest operational update.

On a positive note, it is encouraging to see the acceleration in positive rental reversions, having a significant portion of its loans pegged to fixed rates, and active portfolio management through asset enhancement initiatives.

On the other hand, the decline in occupancy rate may be worrying for some investors.

Following the correction in CapitaLand Ascendas REIT’s share price, it is currently trading at a price-to-book valuation of 1.1x, inline with its historical average.

While CapitaLand Ascendas REIT did not report a dividend in its first quarter operational update, the REIT reported a 4.1% decline in its distribution per unit in the second half of 2023.

Find out how much dividends you would have received as a shareholder of CapitaLand Ascendas REIT in the past 12 months with the calculator below.

Based on CapitaLand Ascendas REIT’s share price of S$2.59 as of 23 April 2024, the REIT offers a dividend yield of 5.9%.

This is similar to Mapletree Industrial Trust’s dividend yield of 5.8%, and lower than Mapletree Logistics Trust’s dividend yield of 6.7%.

Putting these all together, CapitaLand Ascendas REIT does not look like a bargain to me despite its recent share price slide.

If you are keen to understand more about how higher interest rates may impact Singapore REITs, join us for our free webinar on "What's next for Singapore REITs?" on 24th April by registering here.

Join the Beansprout Telegram group to get the latest updates on Singapore REITs, stocks, bonds and ETFs.

Related links:

Join us for a free webinar at 8.00pm on 24th April where we will share what we're looking out for on Singapore REITs.

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Comments

Comments0 comments