Bonds

Is the 1-year T-bill better than the 6-month T-bill and fixed deposits?

By Gerald Wong, CFA • 13 Apr 2024 • 0 min read

The closing yield on the 1-year Singapore T-bill is lower than the 6-month T-bill at 3.54%. However, investors of the 1-year T-bill may face lower re-investment risks.

In this article

What happened?

I have seen more investors discussing about the 1-year Singapore T-bill recently.

Just yesterday, someone in the Beansprout community asked what the yield is likely to be for the upcoming 1-year T-bill.

I also came across the question “Since 6-month T-bill interest rate is at 3.75% vs 1-year T-bill at 3.5%, isn’t it better to buy 6-month T-bill?”

Many investors seem to be eyeing the upcoming 1-year Singapore T-bill (BY24101X) on 18 April 2024.

After all, the yield on the previous 6-month T-bill has remained fairly high at 3.75%, despite the fall in fixed deposit rates.

In this post, I will be looking at some of the latest indicators to find out if it is worthwhile to apply for the 1-year Singapore T-bill.

What is the likely yield on the 1-year Singapore T-bill?

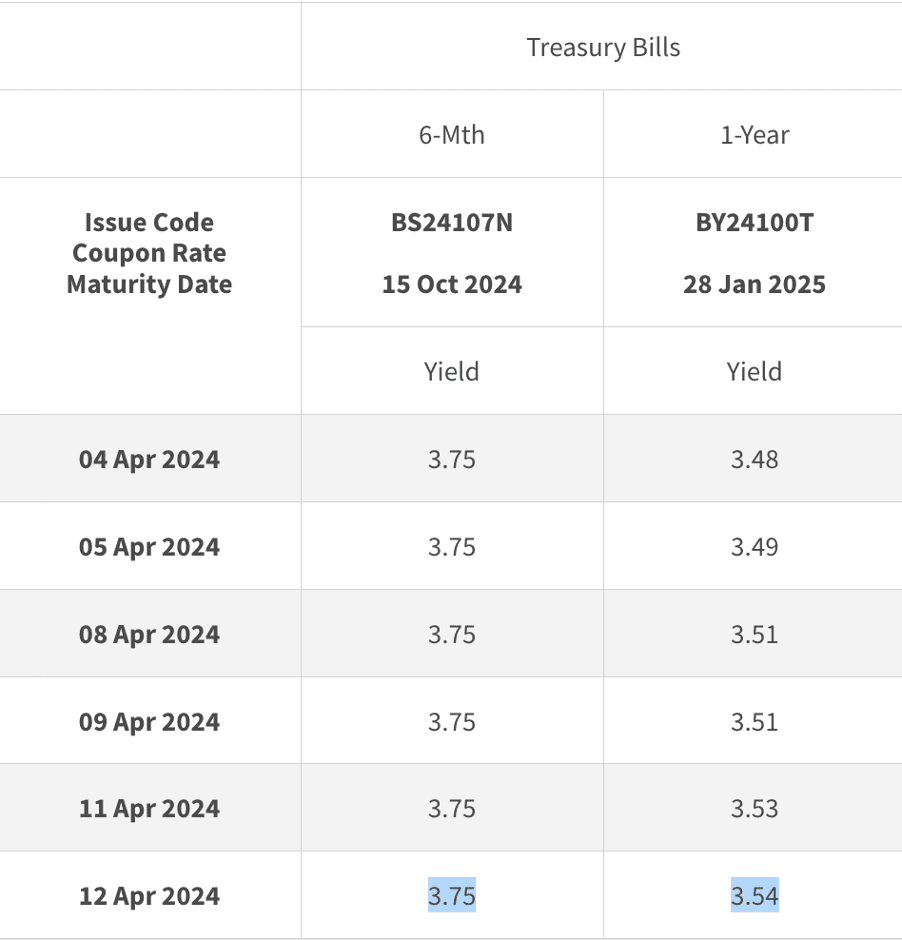

The closing yield on the 1-year Singapore T-bill was at 3.54% on 12 April, based on daily market prices published by the MAS.

The yield has risen slightly over the past week as US government bond yields have jumped on concerns that inflation may remain sticky.

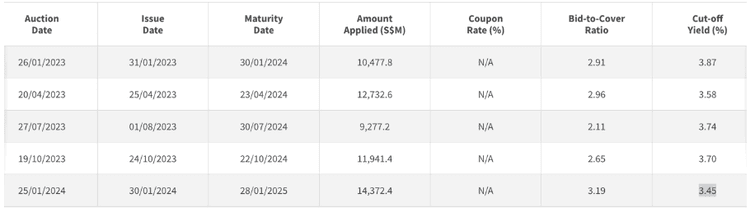

With the increase, the latest closing yield on the 1-year Singapore T-bill would be higher than the cut-off yield of 3.45% in the previous auction in January 2024.

However, it is worth noting that the eventual cut-off yield in the auction may differ from the closing yield.

For example, the cut-off yield in the previous auction was lower as demand for T-bills surged. We have seen an increase in applications for both the 6-month and 1-year T-bill in recent auctions.

Buying Singapore 1-year T-bill – better than 6-month T-bill?

Rather than apply for the 1-year T-bill, one option to consider is to invest in two separate tranches of 6-month T-bill.

Specifically, we can invest in the upcoming 6-month T-bill auction, and re-invest the funds when the T-bill matures in six months’ time.

If we apply for the next 6-month T-bill on 25 April, the maturity of the T-bill will be on 29 October 2024.

The next 6-month T-bill that we can potentially apply for with our funds will be on 7 November 2024, and the 6-month T-bill will mature on 13 May 2025.

Indeed, the closing yield of 3.54% on the 1-year Singapore T-bill would be lower than the cut-off yield of 3.75% for the latest 6-month Singapore T-bill auction.

However, this may not mean that the 6-month T-bill is always better than the 1-year T-bill.

To decide if it is better to buy the 1-year T-bill or the 6-month T-bill, the question I will ask is whether I should lock-in the yield for 12 months, or face potential re-investment risk if government bond yields were to fall sharply in 6-months’ time.

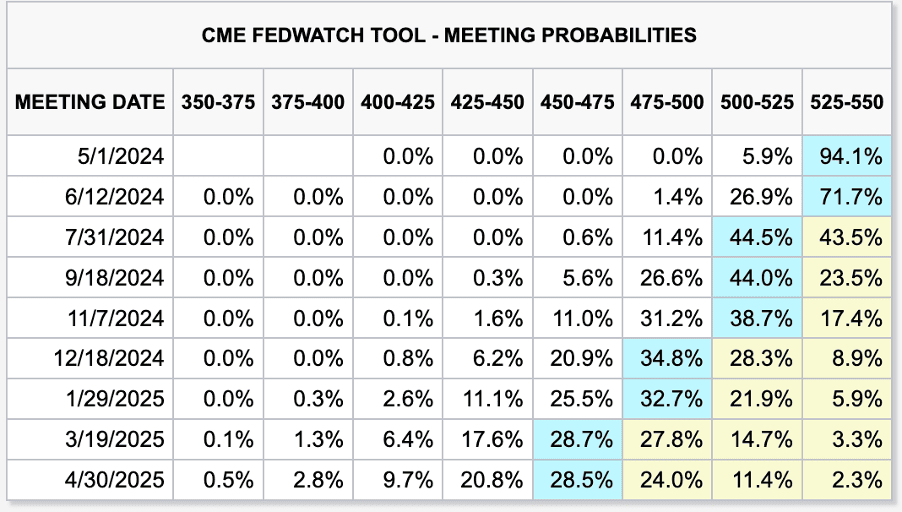

According to the US Federal Reserve’s latest projections in March, there may be three interest rate cuts in 2024.

Investors are currently expecting two rate cuts in 2024, based on the CME Fedwatch Tool as of 13 April 2024.

The first interest rate cut is largely expected in July, with another rate cut potentially in December this year.

If interest rates were to fall sharply in the coming months, we may get a lower yield on the T-bill when re-investing our funds in the 6-month T-bill in November.

Hence, we will have to keep track of interest rate trends in the coming months if we were investing in the 6-month T-bill.

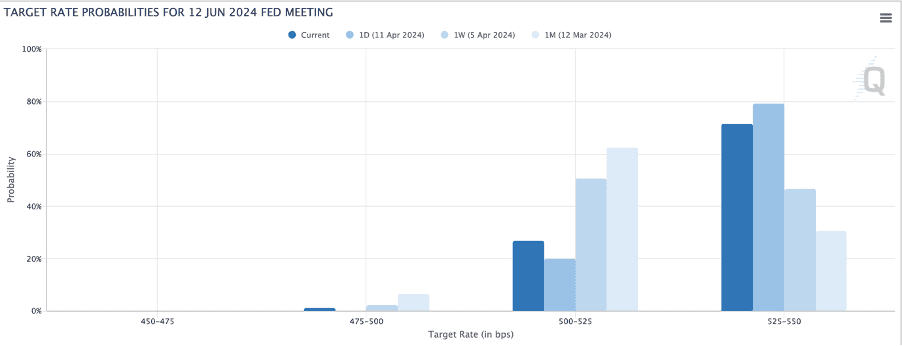

For example, we have seen significant changes in the expectations on the interest rate cuts since the start of the year.

Just last week, investors were expecting that we will see the first interest rate cut in June this year.

However, the likelihood of a rate cut in June has diminished as inflation in the US has remained stubbornly high.

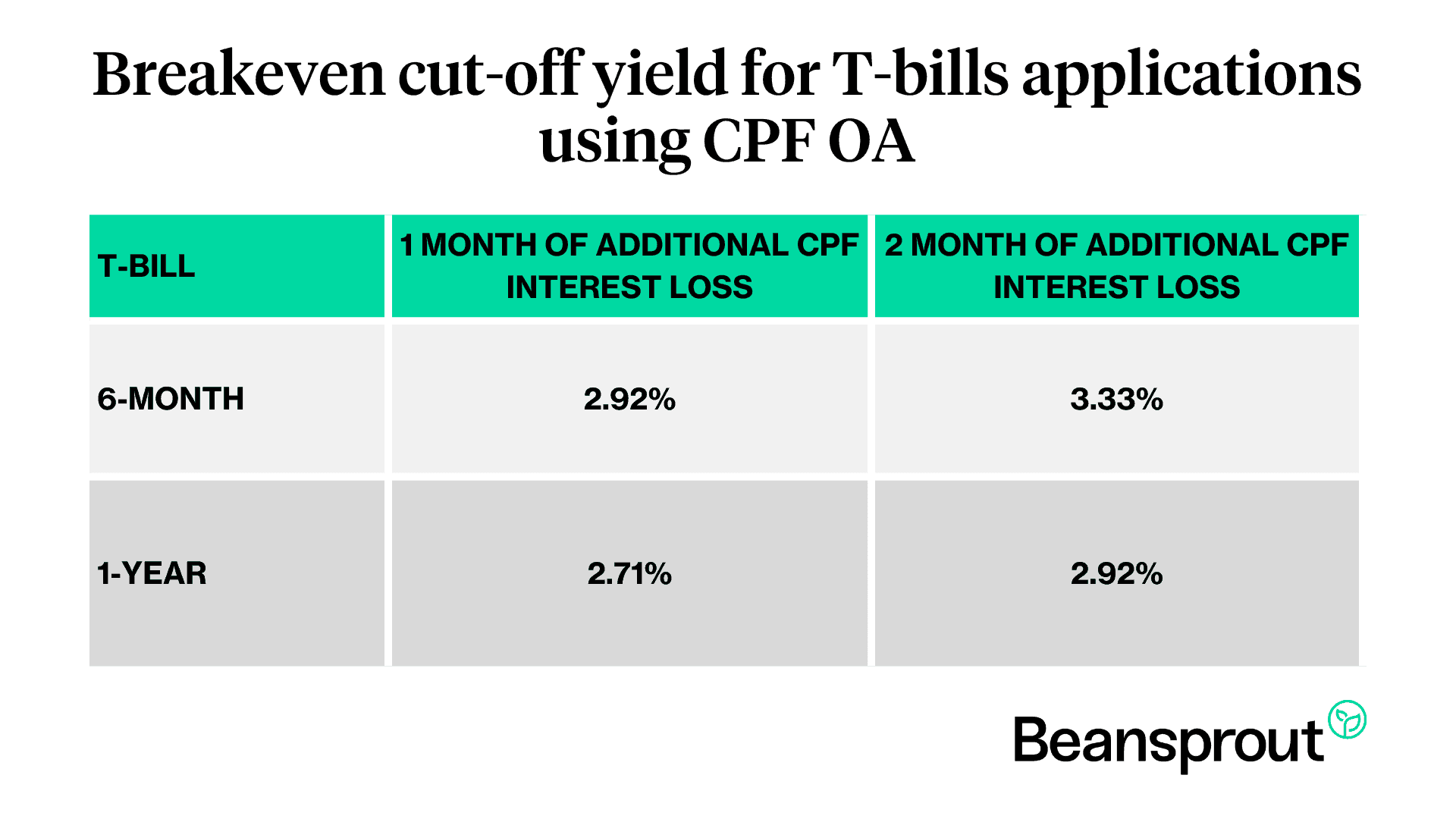

Buying Singapore 1-year T-bill using CPF – Is it worth it?

We shared earlier that due to the loss of CPF interest, it is generally more worthwhile to use your CPF funds to invest in the T-bill when the bond has a longer maturity.

For example, the breakeven cut-off yield for T-bill applications using CPF OA falls to about 2.7% for a 1-year T-bill from 2.9% for a 6-month T-bill, assuming the loss of one additional month of CPF interest.

For the upcoming 1-year T-bill auction on 18 April, the issue date will be 23 April 2024, and the maturity date will be on 22 April 2025.

If we are not looking to re-invest our funds into the next T-bill, we will potentially lose 13 months of CPF interest by investing in the 1-year T-bill using our CPF savings, assuming we transfer funds back to our CPF OA account immediately when the T-bill matures.

On the other hand, we will potentially lose 14 months of CPF interest by investing in two separate tranches of the 6-month T-bill, as the second tranche of the 6-month T-bill will only mature in May 2025.

Buying 1-year T-bill using cash – better than fixed deposit?

Singapore banks have been lowering their fixed deposit interest rates in recent months.

Currently, the best 1-year fixed deposit rate we found is at 3.20% p.a.

This would be lower than the latest closing yield of 3.54% on the 1-year T-bill, as well as the cut-off yield of 3.45% in the previous 1-year T-bill auction.

Also, you can only earn this 12-month fixed deposit rate of 3.2% p.a. with DBS for up to $19,999 of deposits.

However, you would be able to apply for a larger amount of T-bills in the upcoming auction.

What would Beansprout do?

The current closing yield of the 1-year Singapore T-bill of 3.54% is lower than that of the 6-month T-bill.

However, we may still consider the 1-year Singapore T-bill over the 6-month Singapore T-bill to lock in the interest rates and not worry about re-investment risk.

While investors are currently expecting the Fed to delay its interest rate cuts, these expectations may change quickly if inflation were to ease significantly in the coming months.

Another reason that some investors may prefer the 1-year Singapore T-bill over the 6-month T-bill is to reduce the loss of additional CPF interest.

The good news for T-bill investors is that whether you decide to invest in the 6-month or 1-year T-bill, the current closing yields are higher than the best fixed deposit rates.

As such, we would consider the 1-year T-bill as a safe way to earn a higher return on our savings, especially if we are looking to lock in interest rates for a longer period of time compared to the 6-month T-bill.

The auction will be held on Thursday, 18 April 2024. As cash applications for the T-bill close one business day before the auction date, we would need to put in our cash applications for the T-bill by 9pm on 17 April (Wednesday).

Applications for the T-bill using CPF-OA will close 1-2 business days before the auction date, and the dates differ across the three local banks.

- Applications for T-bills online using CPF OA via DBS close at 9pm on 17 April (Wed). Read our step-by-step guide to applying via DBS.

- Application for T-bills online using CPF OA via OCBC close at 9pm on 17 April (Wed). Read our step-by-step guide to applying via OCBC

- Applications for T-bills online using CPF OA via UOB close at 9pm on 16 April (Tue) Read our step-by-step guide to applying via UOB.

If you decide to apply for the 6-month T-bill instead of the 1-year T-bill, the next 6-month T-bill auction will be held on 25 April 2024.

To learn more about T-bills and find out how to apply, check out our Comprehensive Guide to T-bills.

Join the Beansprout Telegram group get the latest insights on Singapore bonds, stocks, REITs, and ETFs.

This article was first published on 13 April 2024 .

Read also

Want to learn more? Discover more Bond-related insights here.

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Comments

Comments0 comments