Stocks

UOB shares fall from 1-year high. What you need to know about its latest earnings

By Gerald Wong, CFA • 08 May 2024 • 0 min read

UOB's share price fell after the bank reported its first quarter earnings. We find out more about the company's prospects from its latest results.

In this article

UOB shares fall from 1-year high. What you need to know about its latest earnings.

I shared earlier in my weekly update that I will be looking out closely for UOB’s results this week.

After all, DBS had reported a record first quarter earnings just last week, pushing its share price to an all-time high.

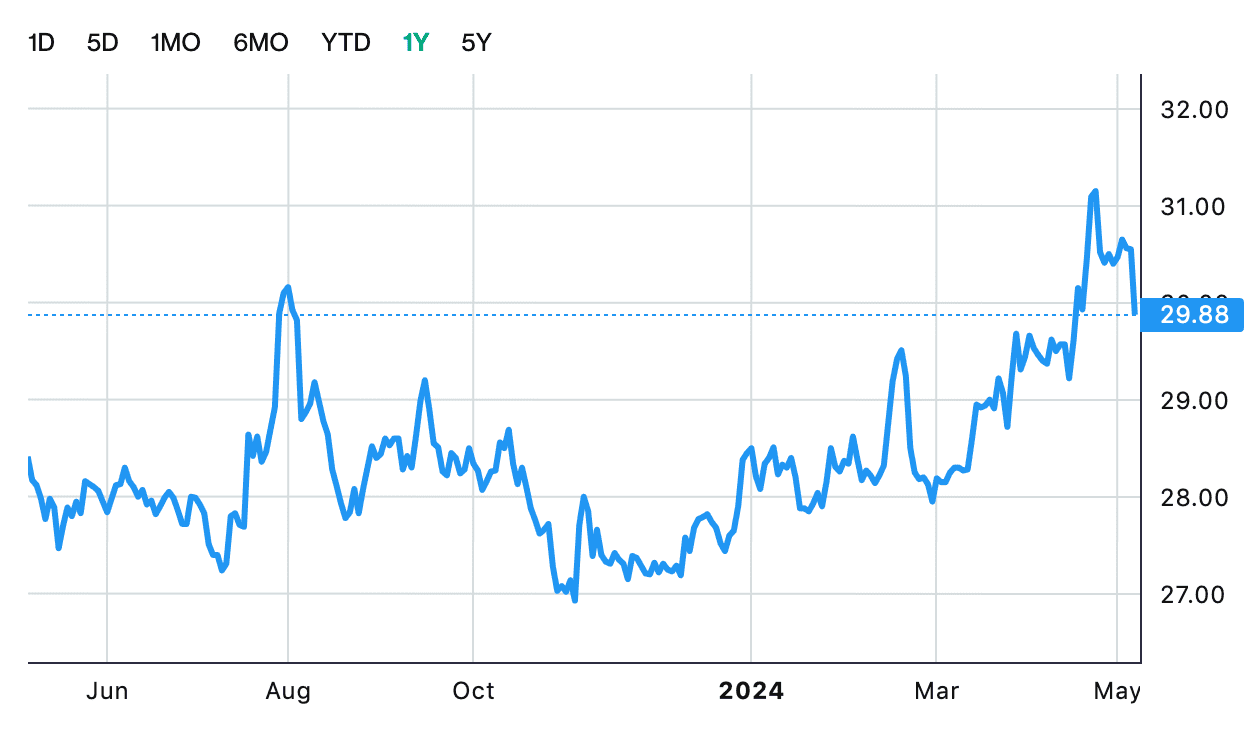

UOB’s share price also recently reached a 52-week high of $31.35, but has declined thereafter as it traded ex-dividend.

Investors also appear slightly disappointed with its first quarter results, as UOB’s share price fell by 2.2% to close at $29.88 on 8 May.

Let us dive deeper to find out more about UOB’s first quarter earnings.

What you need to know about UOB results

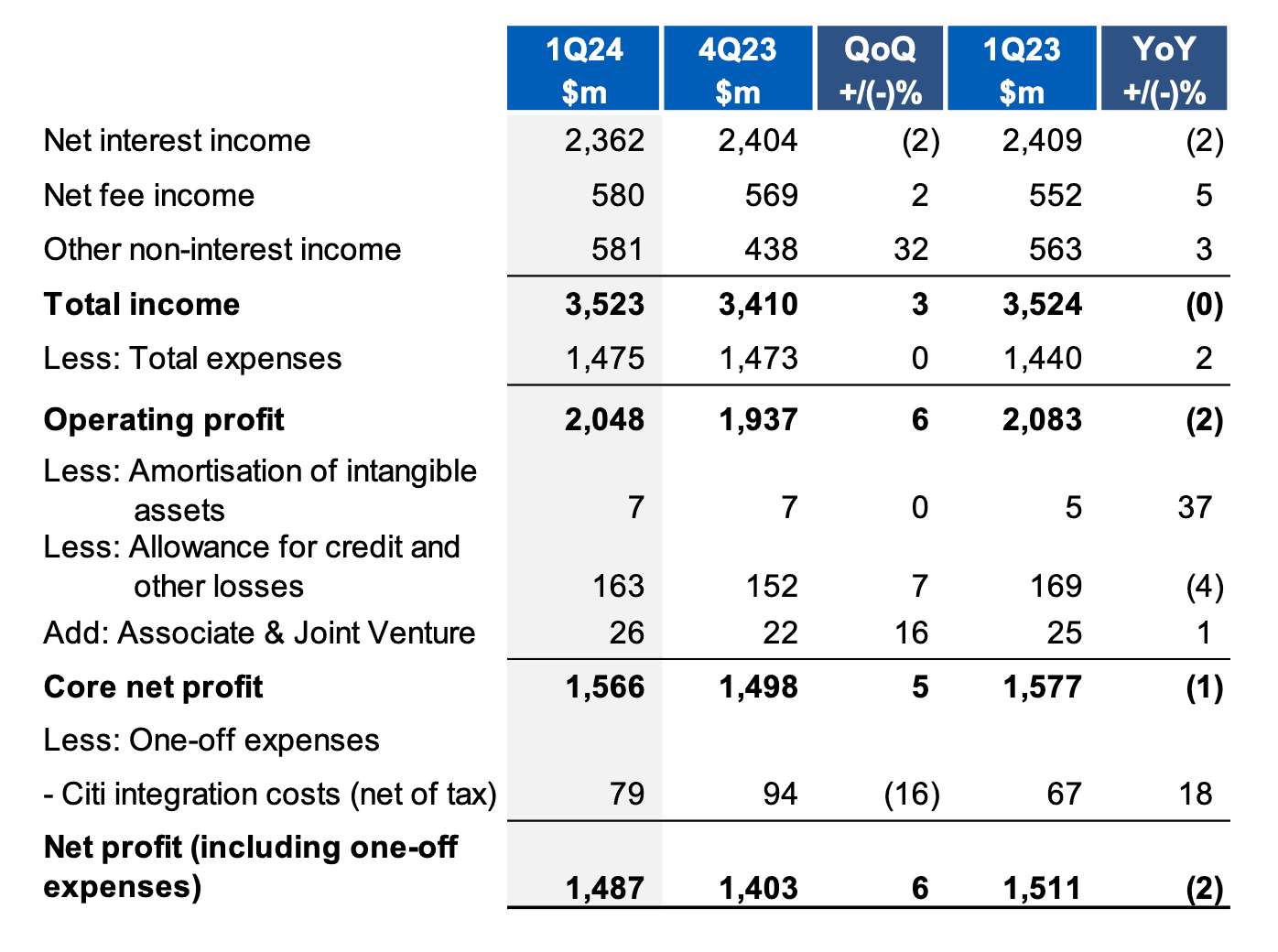

UOB reported a net profit of S$1.49 billion in the first quarter of 2024, a 1.6% decline year-on-year.

Total income was flat compared with previous year, with lower net interest income offset by higher fee income, and income from trading.

Overall, the profit appears to be in-line with market expectations.

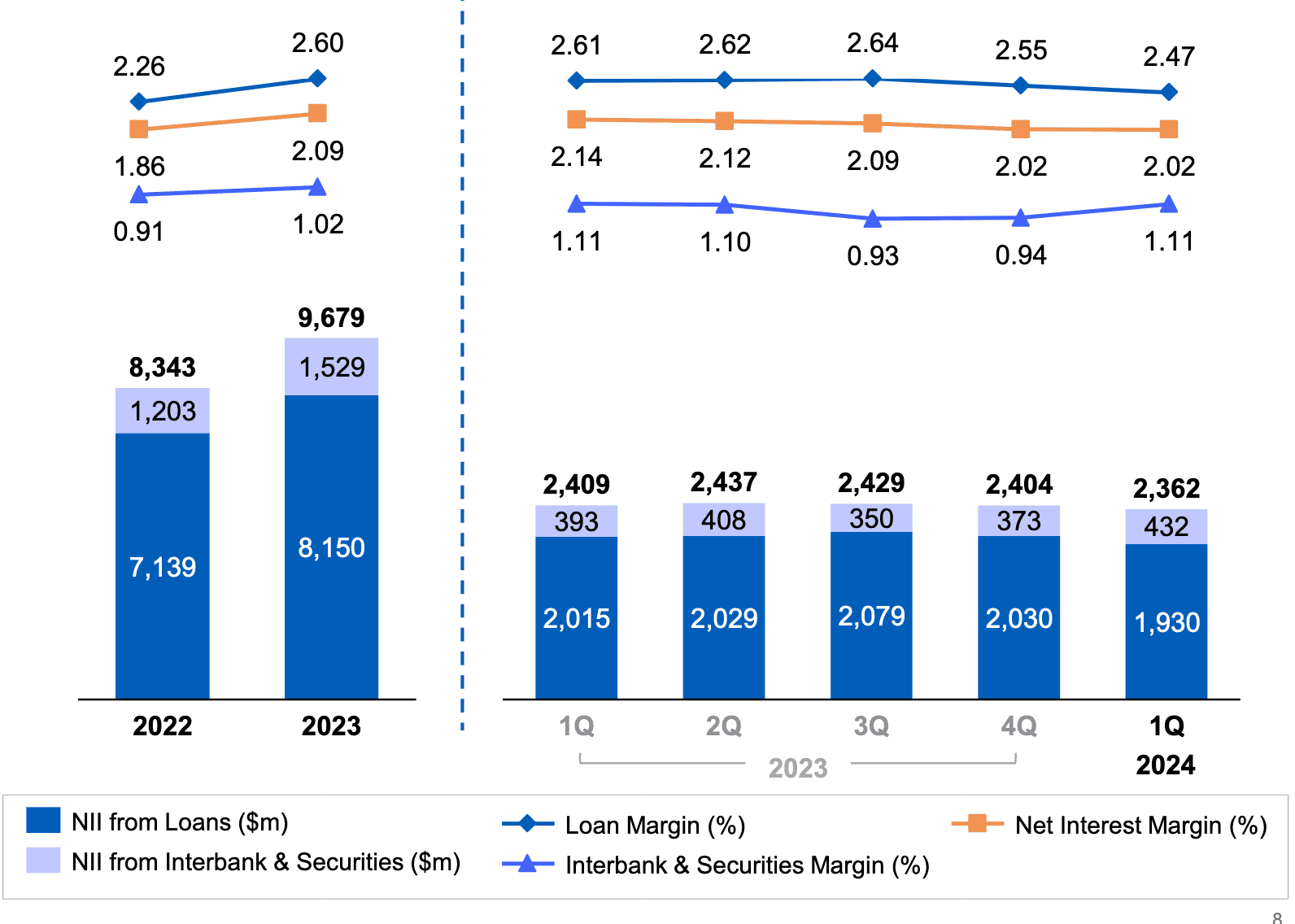

#1 Lower interest margins from loans

Net interest income was 1.7% lower than 4Q23, due to weaker margins from loans.

Net interest margin from loans slipped to 2.47%, from 2.55% in 4Q23, a result of higher cost of fund, and competitive pricing for loans to better-quality customers.

Overall net interest margin was held stable at 2.02%, as the bank raised its investments in longer-dated bonds and government treasury that offer higher yields.

According to UOB’s management, its net interest margin may improve in 2Q24 with lower cost of funds, if UOB’s recent cuts in their fixed deposit (FD) rates can sustain.

At the same time, total deposits in current account and savings accounts as a percentage of total fund (CASA ratio) rose to 50.6%, from 48.9% in 4Q23.

These are lower-cost funding sources, which may help to reduce the cost for the bank.

UOB may need to raise FD rates if the higher-for-longer rate environment persists and the peers do not cut. At the same time, its lending rates may remain under pressure as it prioritizes asset quality. These may then weigh on its net interest margins.

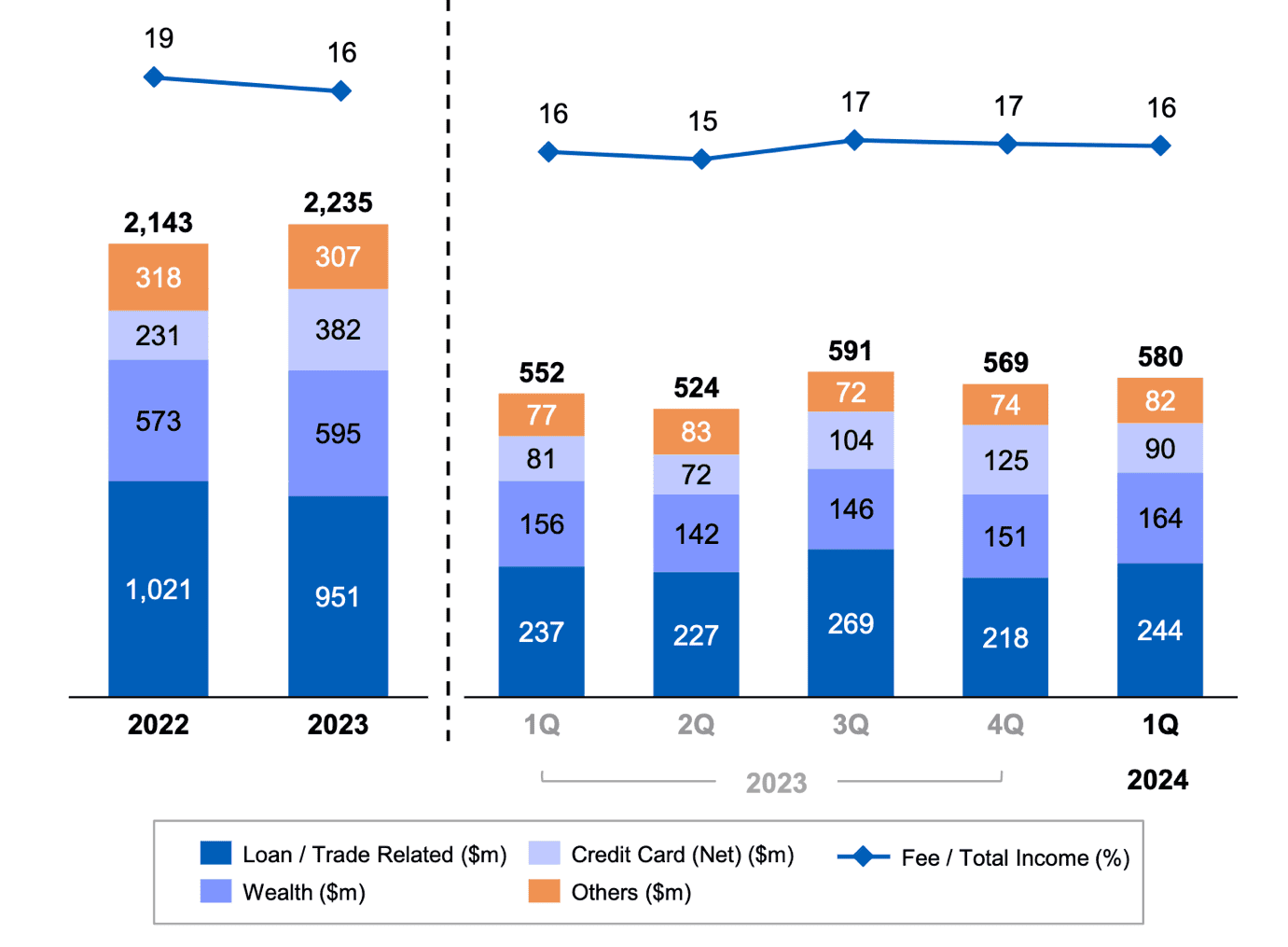

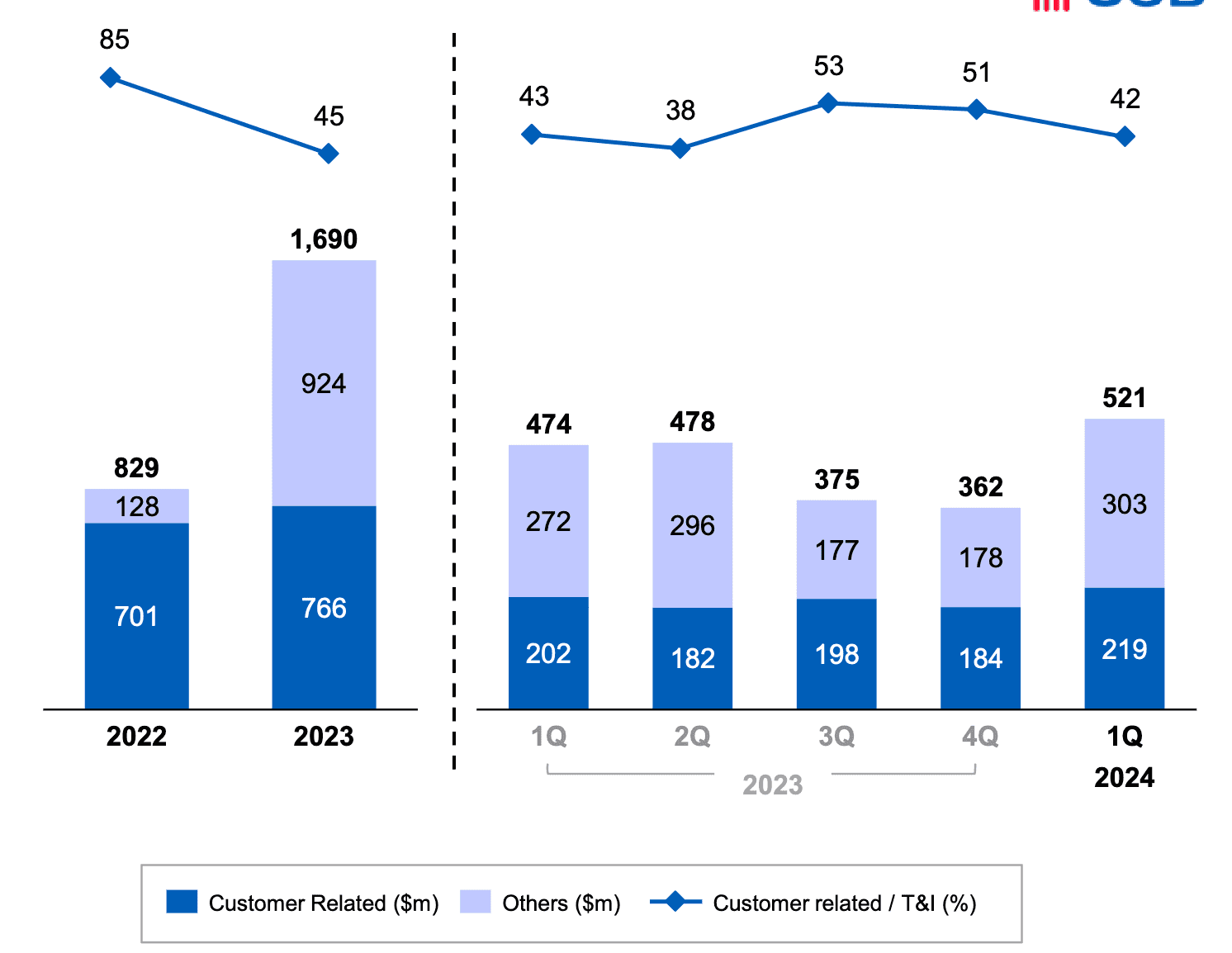

#2 Higher wealth and loan-related fees, card fees disappointed

Fee income grew 5.1% over the previous year, and 2.1% over 4Q23, led by wealth management and loan-related fees.

These segments gained from a bigger asset under management (AUM) of S$179 billion, and with more of these funds deployed into investments. AUM grew S$3 billion during the quarter.

Card fee income disappointed as it fell 28% from 4Q23, considering that the total number of credit/debit cards of the group reached 8 million after the Citi integration.

Still, UOB expects fee income to grow at double digit this year.

#3 Higher trading income, but not recurring

Trading income rose 32.6%, to account for 16.5% of total income (4Q23: 12.8%), possibly due to stronger trading activities in the equity markets. However, this is unlikely to be recurring.

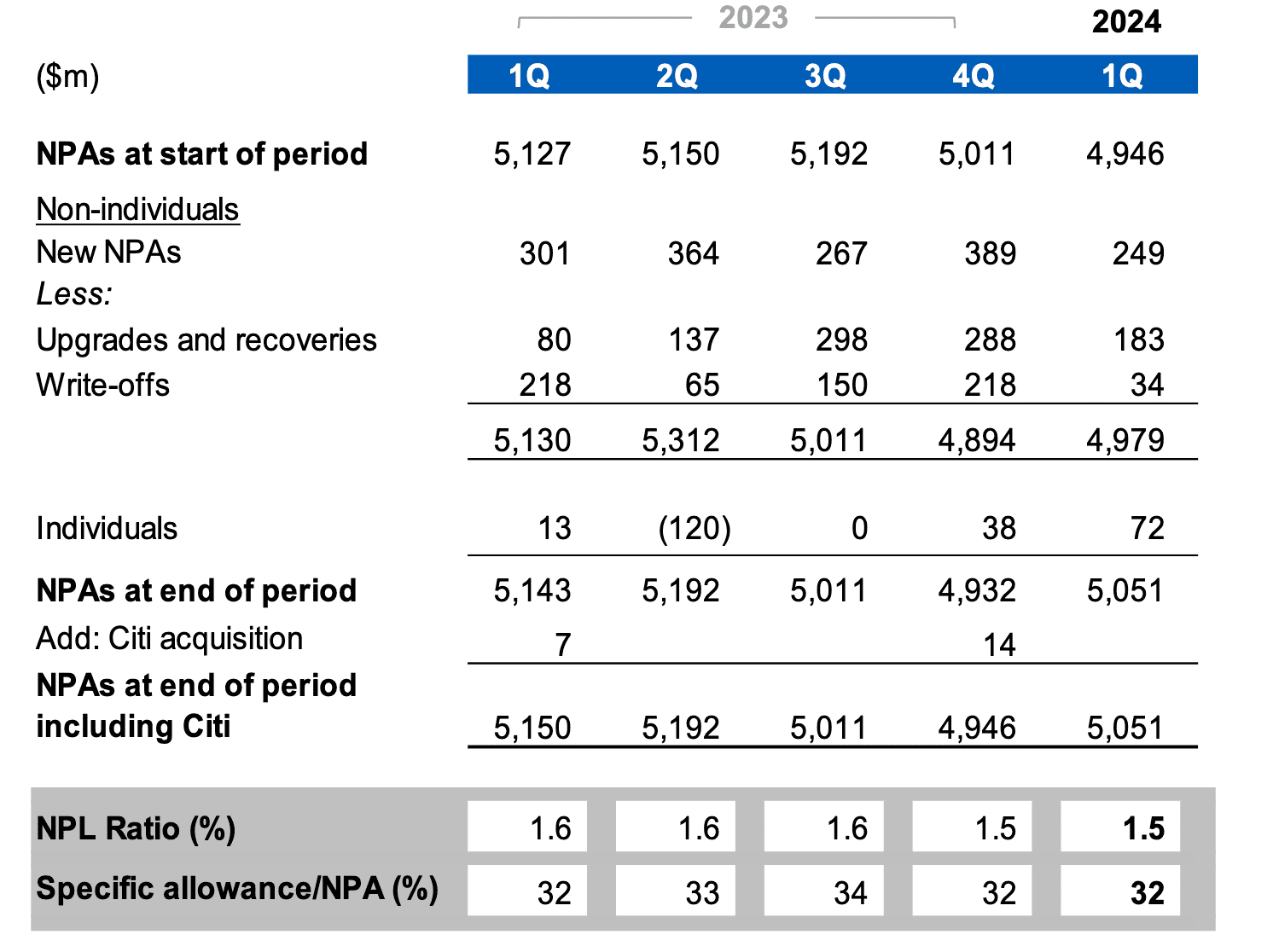

#4 Credit costs, asset quality intact

Total credit cost was 23 basis points, a slight improvement from 25 basis points in 4Q23. Asset quality looks healthy, with non-performing loan ratio maintained at 1.5% of total loans.

Management added that it has not seen any stress in its regional loans books, even with the integration of Citi, as Citi targets the mid to high end consumers.

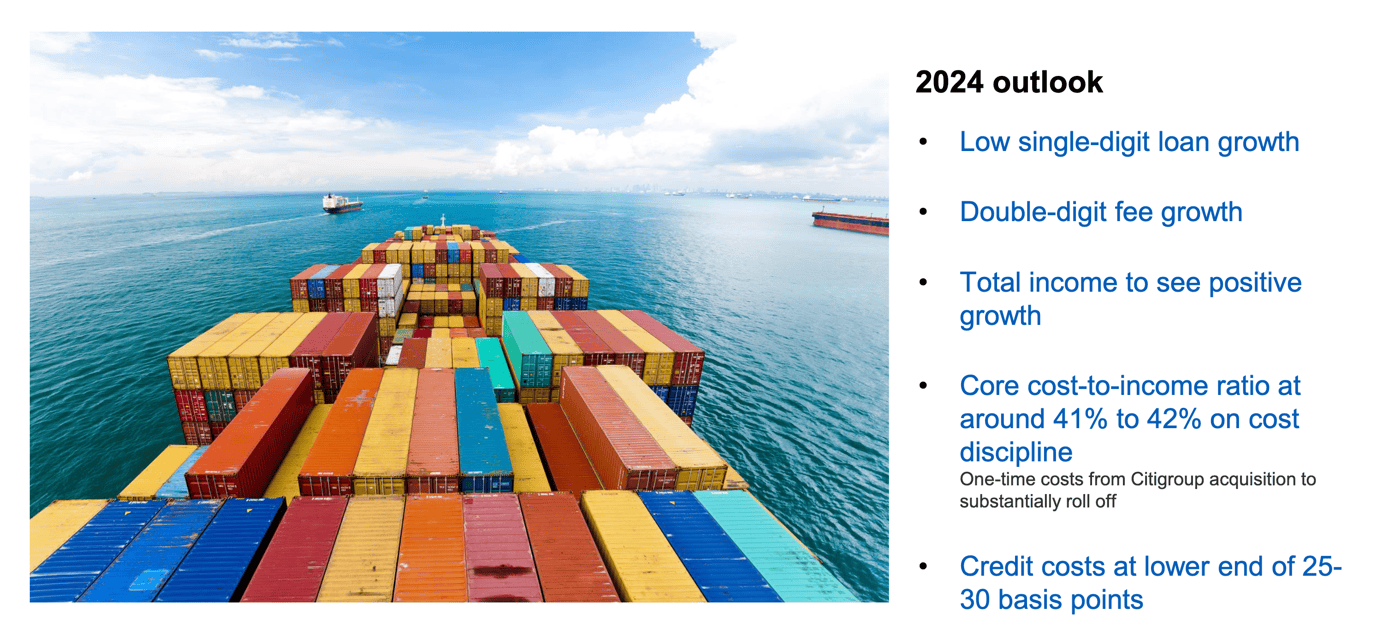

#5 UOB maintained its guidance

Management maintained its guidance:

- It expects a low single-digit loan growth in FY24

- Fee income to grow at double-digit

- Positive growth in total income

- Core cost-to-income ratio at 41-42%. The cost of Citi acquisition will roll off in 2H

- Credit costs at lower end of 25-30 basis points (1Q24: 23 basis points)

What would Beansprout do?

Overall, it seems like UOB has reported a decent set of results as net interest margins held steady, while higher wealth and loan-related fees offset weaker card fees.

While trading income was strong, this is unlikely to be recurring.

At the same time, UOB has kept its guidance for 2024 unchanged.

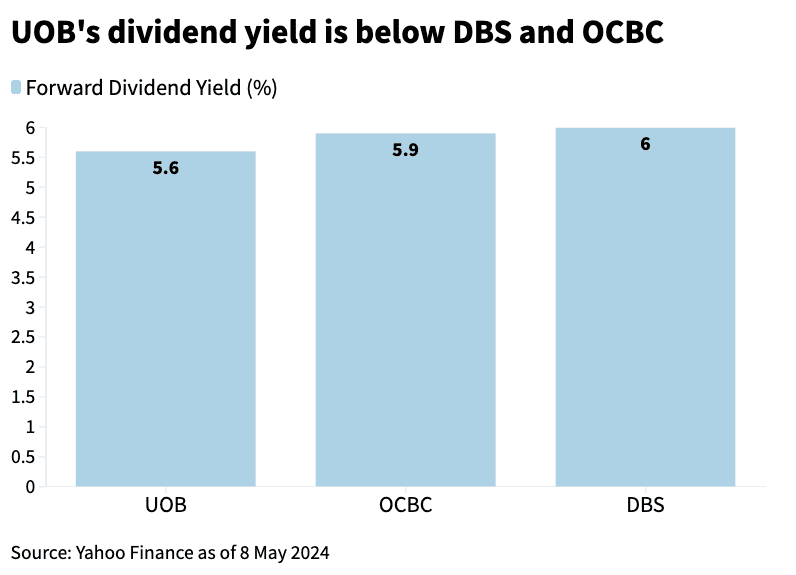

For investors who are looking at UOB for its dividend payout, its strong ROE of 14.0% puts it in good stead to potentially raise its dividends.

However, UOB management stated that it is likely to stick to the 50% dividend payout ratio for now, as it focuses on looking out for new growth opportunity to deploy the excess capital.

Find out how much dividends you would have received as a shareholder of UOB in the past 12 months with the calculator below.

UOB currently offers a dividend yield of 5.6%, slightly below the expected dividend yield of 6.0% for DBS.

As such, DBS might be more worthwhile considering over UOB for investors looking at Singapore banks for their dividend yields.

If you are interested to learn about income opportunities in the Singapore market, join our upcoming webinar on 14 May 2024 to find out how you can identify these opportunities.

Join the Beansprout Telegram group for the latest insights on Singapore stocks, REITs, bonds and ETFs.

Related links:

Read also

Gain financial insights in minutes

Subscribe to our free weekly newsletter for more insights to grow your wealth

Comments

Comments0 comments